Sterling slipped against its major peers on Thursday after the central bank left its monetary policy unchanged, while issuing a modest downgrade to its inflation and growth forecasts.

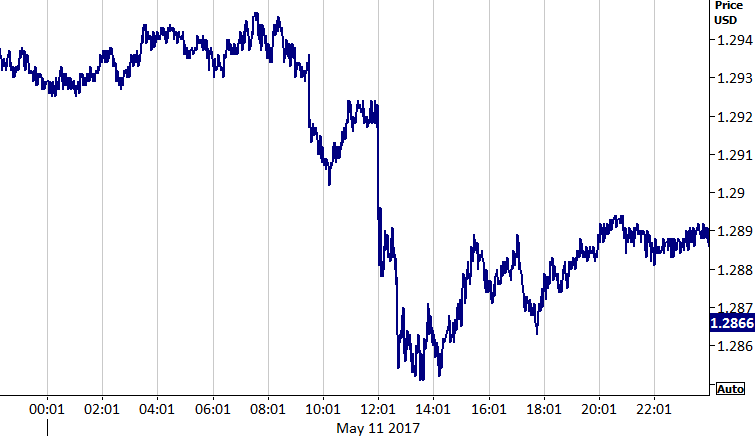

The disappointing lack of an additional dissenter can be attributed to much of the reaction in Sterling, which fell by around half a percent against the Dollar following the announcement (Figure 1). It’s worth noting that Forbes will leave her post on the MPC after the next meeting, which could mean the vote returns to being unanimous again at the August meeting.

Figure 1: GBP/USD (11/05/17)

Currency traders almost completely overlooked the actual communications from the BoE, which were less dovish than the initial market reaction would suggest. The BoE signalled that it may need to hike sooner than the market is pricing in and that it is confident consumer spending and real earnings growth would recover in the long term.

Overall, the BoE appears to be adopting a fairly cautious outlook on rates and we think they are in no rush to hike unless there is a significant unexpected increase in inflation above around the 3% mark. That being said, market pricing for a rate increase this year is still slightly on the low side (around 25%), given domestic prices are rising and the economy is glowingly relatively solidly.

Away from the UK, the Euro slipped to a three week low against the US Dollar as investors continue to unwind bullish bets on the currency following the French Election. We now look to this afternoon’s inflation data out of the US as the main announcement in the calendar today.

Major currencies in detail

GBP

GBP

Yesterday’s disappointing lack of an additional dissenter was compounded by the central bank downgrading its inflation, which it now expects to reach 2.6% next year and 2.2% in 2019.

Governor Mark Carney continued to emphasise that the increase in consumer prices was driven almost exclusively by the depreciation in Sterling, which the central bank is likely to overlook. However, we think there is a limit as to how much of an inflation overshoot the Bank will tolerate before it begins discussing higher rates.

With the Bank of England meeting now out of the way, investors turn their attention back to the General Election with just under a month until polling day.

EUR

The Euro slipped against the US Dollar yesterday, expending its losses since the French election to around 1.3% despite the release of the latest growth forecasts from the European Commission.

The European Commission raised its prediction for growth in 2017 in the Euro-area to 1.7% from 1.6%. This reflects the generally better-than-expected economic news out of the currency bloc that has caused many analysts to bring forward their expectations for when the ECB will abandon its ultra-dovish monetary policy stance.

Industrial production numbers this morning are expected to show output in the sector accelerated in March, following a slightly underwhelming February.

USD

Federal Reserve member William Dudley spoke in the US yesterday, claiming that the central bank will gradually reduce reinvested assets “sometime later this year or next year”. Communications from policymakers in the US remains fairly hawkish, suggesting to us that there remains a realistic possibility that the Fed could hike interest rates as many as four times this year. Boston Fed President Eric Rosengren reiterated that he backs three more hikes this year.

Investors will be firmly focusing on the release of the latest retail sales and inflation numbers out of the US this afternoon. Headline inflation is expected to show a modest down tick to 2.3% from 2.4%.